For banks, a white-labelled wallet can provide a fast, cost-effective way to bring innovative digital payment services to market. But their customers can benefit significantly too.

As Markus Coradi, Head of Digital Business & Innovation at Viseca noted after integrating G+D Netcetera's ToPay Mobile Wallet, “By focusing on user-friendliness, state-of-the-art technology and innovative features, our app has become a favourite of over two million users.”

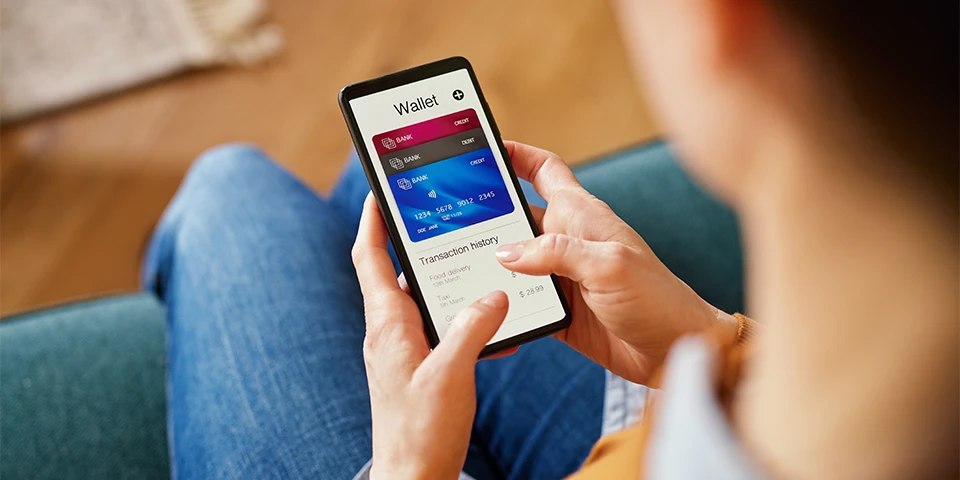

A feature-rich digital wallet also results in customers enjoying a more convenient digital payment experience.

Atila Selim, Head of Alternative Distribution Channels Marketing at Halkbank, explains the impact of choosing a white-labelled mobile wallet: “G+D Netcetera's ToPay wallet enables us to offer customers secure, easier and faster digital payments. This is a big step in terms of digital transformation of banking in the region.”

On a broader level, the adoption of digital wallets advances the digitalisation of payments and banking. Contactless payments improve hygiene and reduce friction, digital cards reduce waste and improve security, and instant payments offer an alternative to cash, contributing to the gradual shift toward a cashless society.